How To Enroll in Medicare in Utah

Table of Contents

Enrolling in Medicare does not have to be complicated, but getting the timing and details right matters, especially when navigating plan options available in Utah. Whether you are turning 65 or new to Medicare, this guide walks you through eligibility, enrollment periods, costs, and what happens after you sign up.

If you are not sure what Medicare is or how it works, start there before diving into enrollment.

Who Qualifies for Medicare in Utah: Eligibility Requirements

Medicare is a federal health insurance program primarily designed for people age 65 and older. To be eligible for Medicare in Utah, you must be a U.S. citizen or a lawful permanent resident who has lived in the United States for at least five continuous years.

However, turning 65 is not the only path to Medicare. You may also qualify if you are under 65 and meet one of these criteria:

- You have received Social Security Disability Insurance (SSDI) benefits for 24 months

- You have been diagnosed with Amyotrophic Lateral Sclerosis (ALS), also known as Lou Gehrig's disease. Medicare begins the same month your SSDI benefits start

- You have End-Stage Renal Disease (ESRD) and need regular dialysis or a kidney transplant

If you are not sure whether you qualify, the Social Security Administration website has tools to help you check your eligibility status.

"A common misconception about Medicare is that you must be retiring and collecting Social Security to enroll. Medicare and Social Security are separate programs. You can enroll in Medicare without starting your Social Security benefits," says Nikki Cortinas, a licensed Medicare agent in Texas.

When to Enroll: Your Enrollment Periods

Timing is one of the most important parts of Medicare enrollment in Utah. Missing a deadline can mean gaps in coverage and permanent premium penalties.

Initial Enrollment Period (IEP): This is a seven-month window that includes the three months before the month you turn 65, the month of your 65th birthday, and the three months after. This is your primary opportunity to sign up without penalty.

"If you're turning 65, you'll first enroll during your Initial Enrollment Period, a 7-month window that starts 3 months before your birthday month, includes your birthday month, and ends 3 months after," says Stephanie Calvillo, a licensed Medicare agent in Texas. "There's also a Medicare Advantage Open Enrollment Period from January 1 through March 31 if you already have a Medicare Advantage plan and want to switch or make changes."

General Enrollment Period (GEP): If you miss your IEP, you can sign up between January 1 and March 31 each year. Coverage starts the first day of the month after you enroll. Previously, coverage was delayed until July 1, but the rule was updated to give faster access to benefits. You may still face a late enrollment penalty that increases your premiums permanently, one of the most common Medicare mistakes to avoid.

"The worst Medicare-related decision someone can make is not enrolling on time when they are first eligible and do not have other creditable coverage," says Tory Blain, a licensed Medicare agent in Utah. "Missing the right enrollment window can lead to late enrollment penalties, delayed coverage, and expensive gaps in care that could have been avoided. Before delaying Medicare, make sure your current coverage allows you to postpone enrollment without penalties or problems later."

Special Enrollment Period (SEP): If you delayed Medicare because you had coverage through an employer in Utah, you may qualify for a Special Enrollment Period. You can also learn more about Special Enrollment Period eligibility to see if your situation qualifies. Be sure to understand your Medicare Advantage enrollment periods as well if you are considering that route.

According to Mindy Berry, a licensed Medicare agent in Ohio, "You are not required to sign up for Medicare if you have creditable coverage with your employer health coverage. When you decide to move to Medicare or when you retire, you will need to have a form signed by your employer stating that you have been insured since turning 65. It is a good idea to compare your employer coverage with Medicare to see which plan is better for you and your lifestyle."

Beyond these periods, Medicare Open Enrollment runs from October 15 through December 7 each year and allows Utah residents to make changes to their existing Medicare coverage for the following year.

What Medicare Costs to Expect

Understanding costs upfront helps Utah residents budget and avoid surprises. For a full breakdown of every premium, deductible, and out-of-pocket expense, see our guide to how much Medicare costs in 2026.

- Part A (Hospital Insurance): Most people pay $0 in premiums for Part A if they or their spouse paid Medicare taxes for at least 40 quarters (10 years). If you do not qualify for premium-free Part A, see our breakdown of Part A costs, premiums, and deductibles for the full picture.

- Part B (Medical Insurance): The standard Part B premium in 2026 is $202.90 per month. Higher earners pay more through Income-Related Monthly Adjustment Amounts (IRMAA).

- Late Enrollment Penalties: If you do not sign up for Part B when you are first eligible and you do not have qualifying employer coverage, you will pay a 10% penalty for each 12-month period you could have had Part B but did not. This penalty is added to your monthly premium for as long as you have Part B. Part D works differently: the penalty is roughly 1% of the national base beneficiary premium multiplied by the number of months you went without creditable drug coverage, and it also lasts for as long as you have Part D.

"Seniors end up with lifelong penalties for Part B or Part D when they go without creditable coverage and don't realize they were supposed to enroll. Medicare charges these penalties to discourage people from waiting until they get sick to sign up, but most penalties happen simply because no one explained the rules to them," says Françoise Mueller, a licensed Medicare agent in Utah. "They didn't know their employer coverage wasn't creditable. They missed their Initial Enrollment Period at 65. They thought, 'I'm healthy, I don't need it yet.' These penalties are permanent. They last for as long as the person has Medicare."

Beyond premiums, you will also have deductibles, copayments, and coinsurance depending on what Medicare covers and which plan you choose. Utah residents looking to reduce out-of-pocket costs may also want to explore Medicare Savings Programs that can help pay for premiums and cost-sharing.

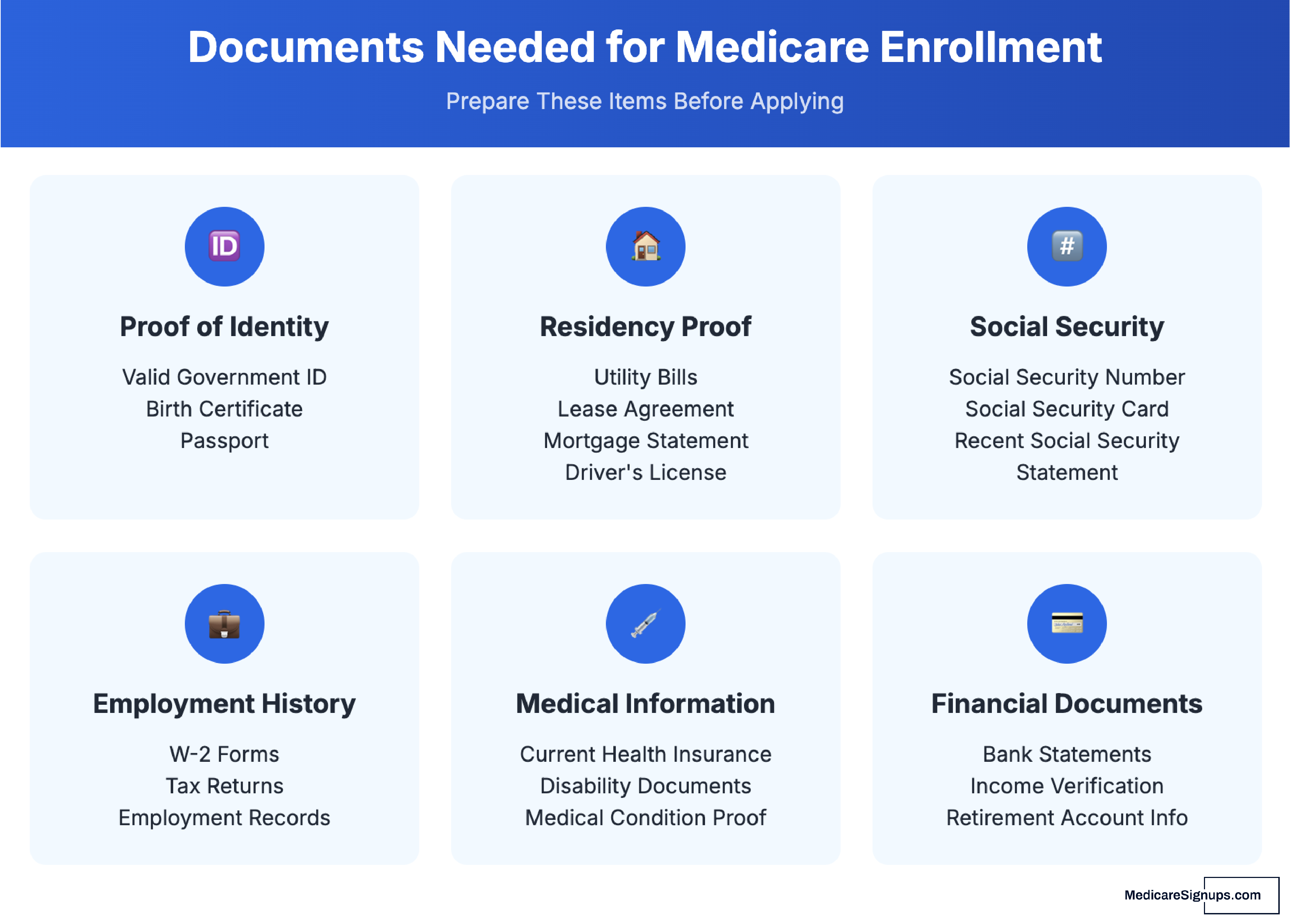

What You Need to Enroll

To enroll in Medicare, you will need to provide certain information, such as your name, date of birth, and Social Security number. You may also need to provide proof of your citizenship or permanent residency. For a step-by-step walkthrough, see our guide on how to apply for Medicare.

How to Apply for Medicare in Utah: 4 Ways to Sign Up

There are several ways to apply for Medicare in Utah depending on your situation:

Automatic enrollment: If you are already receiving Social Security benefits when you turn 65, you will be automatically enrolled in Medicare Parts A and B. Your Medicare card will arrive in the mail about three months before your 65th birthday, and no separate application is needed.

Online: Visit www.ssa.gov and apply through your my Social Security account. You can apply for Part A alone, Part B alone, or both at once. The online application takes about 10 minutes and you will receive a confirmation number immediately.

By phone: Call Social Security at 1-800-772-1213 (TTY 1-800-325-0778). Representatives are available Monday through Friday, 8 a.m. to 7 p.m. local time.

In person: Visit your local Social Security office in Utah. You can find the nearest office at ssa.gov/locator.

Choosing a Medicare Plan in Utah

Once you have enrolled in Medicare, you will need to choose a plan. The decision can feel overwhelming, especially because newly Medicare-eligible adults get bombarded with junk mail from insurance carriers competing for their business.

"The Medicare mail can definitely be overwhelming when you're turning 65. The biggest thing to remember is that most of what you're receiving is advertising, so don't feel pressured to respond to every piece of mail," says Joel Hill, a licensed Medicare agent in Mississippi. "I usually tell people to throw out the noise and focus on what actually matters to their situation. Medicare isn't one size fits all."

There are essentially two paths:

Path 1, Original Medicare (Parts A and B): This is the traditional fee-for-service program run directly by the federal government. You can see any doctor or hospital that accepts Medicare. Many Utah residents pair Original Medicare with a Medicare Supplement (Medigap) plan to help cover out-of-pocket costs, plus a standalone Medicare Part D Prescription Drug Plan for medication coverage. If Medigap is on your radar, pay attention to your Medigap Open Enrollment Period. It is a one-time six-month window that starts the month your Part B coverage begins, and during that stretch insurers cannot deny you a policy or charge you more based on preexisting conditions in Utah.

Path 2, Medicare Advantage (Part C): These are all-in-one plans offered by private insurance companies in Utah. Most Medicare Advantage plans include prescription drug coverage and may offer extras like dental, vision, and hearing. The trade-off is that you typically must use a plan network of doctors and hospitals. Learn more about the types of Medicare Advantage plans available.

To compare Medicare plans side by side, visit www.medicare.gov or work with a Medicare Agent in Utah who can help you evaluate your options at no cost to you.

What Happens After You Enroll

After your enrollment is processed, here is what to expect:

- Your Medicare card: You will receive your red, white, and blue Medicare card in the mail. Keep it in a safe place. You will need it at doctor visits and when enrolling in additional coverage.

- Coverage start date: When your coverage begins depends on when you signed up during your IEP. If you enrolled in the three months before your 65th birthday, coverage typically starts the first day of your birthday month. If you enrolled during your birthday month or any of the three months after, coverage starts the first day of the month following your enrollment.

- Next steps: Decide whether to stay with Original Medicare or switch to a Medicare Advantage plan. If you keep Original Medicare, consider adding a Medigap policy and a Part D plan. Review the preventive services covered by Medicare so you can take advantage of them right away. Stay informed about upcoming changes to Medicare that may affect your coverage and costs.

Enrolling in Medicare in Utah is a milestone, but it does not have to be overwhelming. Take advantage of your enrollment periods, understand the costs involved, and do not hesitate to reach out to a licensed Utah agent or visit medicare.gov if you need help navigating your options.

Justin Lamoreaux

Licensed Utah Medicare Agent

Contact Justin through Medicare Agents Hub »

Medicare doesn't have to be complicated.

I'm Justin, and I help people cut through the confusion and find coverage that fits their needs and budget. Whether you're new to Medicare or exploring better options, I'll take the time to answer your questions and help you make a confident decision.

My goal is simple: make Medicare easy to understand and help you find the right plan without the stress.

Matt Feret

Author, Prepare for Medicare - The Insider’s Guide

https://prepareformedicare.com

Matt Feret is the author of the Prepare for Social Security - The Insider’s Guide and the Prepare for Medicare - The Insider’s Guide book series and launched PrepareforSocialSecurity.com to help people get objective answers to questions about Social Security and Medicare. Matt is also the host of The Matt Feret Show. He has held leadership roles at numerous Fortune 500 Medicare health insurers in sales, marketing, operations, product development, and strategy for over two decades.